I’m going to save you a massive headache right now. The number one reason investors lose deals isn’t bad negotiation or overpaying—it’s not being ready when the right property shows up.

You find the perfect rental property. The numbers work. You make an offer. And then you scramble to get your mortgage sorted out while the seller entertains other offers. Three weeks later, you’ve lost the deal because your paperwork was a mess and you couldn’t close in time.

Don’t be that person.

Getting pre-approved for an investment property mortgage is different from getting pre-approved for a home you’re going to live in. The documentation is heavier. The income math is more complex. And the lender scrutiny is turned up a notch because, in their eyes, investment properties carry more risk.

Here’s the complete checklist to get this done right, so when you find your deal, you can move fast and close with confidence.

Pre-Approval vs. Pre-Qualification: Know the Difference

Before we get into the documents, let’s clear something up because these terms get thrown around like they mean the same thing. They don’t.

Pre-qualification is a casual conversation. You tell the broker your income, debts, and down payment amount, and they give you a rough idea of what you might qualify for. No documents are verified. No credit is pulled. It’s basically an educated guess. Useful for early planning, but it doesn’t carry any weight when you’re making an offer.

Pre-approval is the real thing. The lender actually verifies your income, reviews your documents, pulls your credit, and gives you a conditional approval for a specific mortgage amount. It’s not a guarantee—they still need to approve the property itself—but it’s a serious indication that your financing is in place.

For investment properties, you want the pre-approval. Every time. Sellers and their agents take pre-approved buyers more seriously, and you’ll know exactly what your budget is before you start making offers. Discover how smart lender choices boost pre-approvals and close more deals for real estate investors.

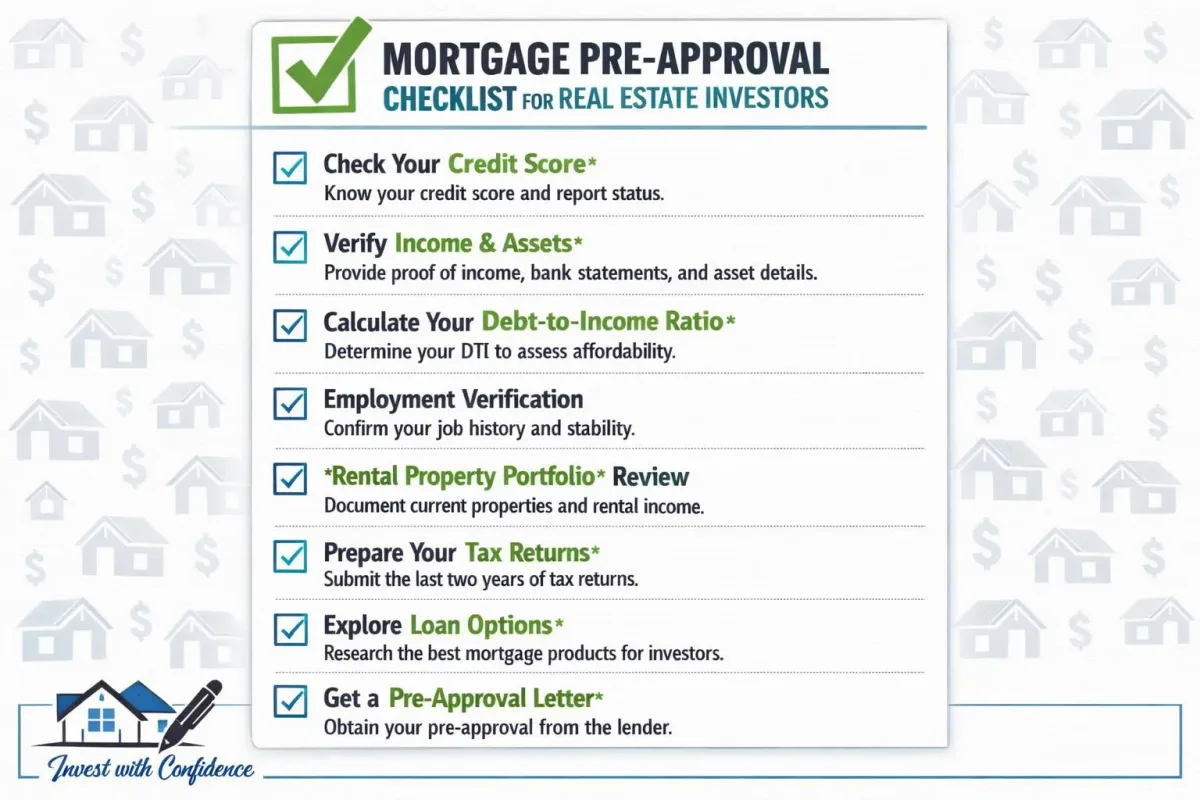

The Document Checklist

Here’s everything you need to gather before you sit down with your mortgage broker. Get all of this ready in advance and you’ll cut your pre-approval timeline significantly.

Income Verification

If you’re employed (T4 income):

- Most recent two years of T4 slips

- Most recent pay stub (within 30 days)

- Letter of employment stating your position, salary, and start date

- If you receive bonuses or overtime, two years of history showing consistency

If you’re self-employed:

- Two most recent years of T1 Generals (full tax returns, not just the summary)

- Two years of Notice of Assessments from CRA

- Business financial statements (if incorporated)

- Articles of Incorporation (if applicable)

- Most recent six months of business bank statements

If you have existing rental income:

- Current lease agreements for all rental properties

- T776 Statement of Real Estate Rentals from your last two tax returns

- Property tax bills for each rental property

- Insurance certificates for each rental property

This is where it gets interesting for investors. Your existing rental income can help you qualify for the next property, but how much it helps depends entirely on the lender’s calculation method. More on that in a minute.

Asset Documentation

- Most recent 90 days of bank statements showing your down payment

- Investment account statements (RRSP, TFSA, non-registered)

- If using gifted funds, a signed gift letter from the donor plus proof of their ability to gift

- Proof of any other assets (vehicles, other real estate, etc.)

Important: Lenders want to see that your down payment has been sitting in your account for at least 90 days. If you recently moved money around, expect questions. Large unexplained deposits raise red flags. If your parents or someone else gifted you money, get that documented properly before you apply.

Property and Debt Information

- Current mortgage statements for every property you own

- Property tax notices for all properties

- Condo fee documentation (if applicable)

- Details of all debts: credit cards, car loans, lines of credit, student loans

- Most recent credit card and loan statements

Identification

- Two pieces of government-issued ID

- Proof of Canadian residency or citizenship status

- Social Insurance Number

Every borrower’s situation is different, and the wrong mortgage structure can cost you thousands — book a free strategy call with LendCity to make sure you’re set up properly.

For a deeper look at the financing angle behind this topic, see our private mortgage investing guide.

How Income Calculation Works for Investors

This is the part most beginners don’t understand, and it’s arguably the most important piece of the puzzle.

When you apply for an investment property mortgage, the lender needs to figure out if you can handle the payments. They look at your total income, subtract your total debts (including all existing mortgages), and see if there’s enough room to add another mortgage payment.

Here’s where rental income enters the picture. The lender won’t count 100% of the rent your properties generate. They apply a discount factor because vacancies and expenses are real. But the percentage they use varies by lender:

| Calculation Method | How It Works | Effect on Qualification |

|---|---|---|

| Rental offset (add-back) | Adds a percentage of rental income (typically 50-80%) to your gross income | Most favorable for qualifying |

| Rental offset (subtraction) | Subtracts mortgage payments from rental income, uses net figure | Middle ground |

| Full debt service | Counts full mortgage payment as debt, limited rental income credit | Most restrictive |

The difference between these methods can be enormous. On a property renting for $2,500/month with a $1,800 mortgage payment, one lender might add $2,000 to your income (80% add-back) while another only credits you $700 (the net after subtracting the mortgage). That gap could mean qualifying for your next property or getting declined.

This is exactly why your broker choice matters so much. A broker who understands these differences will match you with the lender whose math works best for your situation.

GDS and TDS Ratio Limits

Lenders also measure Gross Debt Service (GDS) and Total Debt Service (TDS). GDS compares housing costs to income; TDS includes all debt obligations. Most A lenders cap GDS around 39% and TDS around 44% for investment properties, though exact thresholds vary by lender and product.

Investment property ratios are calculated differently than for a primary residence. Some lenders apply rental income offsets; others add the full mortgage payment to your debt load. These differences directly affect how much you can borrow on your next deal.

Property Type Considerations

Not all investment properties are treated equally by lenders. The type of property you’re buying affects your down payment requirements, interest rates, and even which lenders will fund the deal.

Single-family homes (1 unit): The most straightforward. 20% minimum down payment for a non-owner-occupied investment. Most lenders are comfortable with these.

Duplexes (2 units): Still relatively straightforward. 20% down if you’re not living in it. If you’re planning to live in one unit and rent the other, you might qualify for as little as 5% down with mortgage insurance—a huge advantage for first-time investors.

Triplexes and fourplexes (3-4 units): This is where things start to shift. Some lenders treat these the same as smaller properties. Others want 25% down. A few won’t touch them at all. Your broker needs to know which lenders are comfortable with these.

Five units and above: You’ve crossed into commercial lending territory. Different rules, different lenders, different qualification criteria. The property’s income becomes more important than your personal income. This is a whole different conversation, but your broker should be able to guide you through it when the time comes.

Condos: Lenders care about more than just your finances with condos. They’ll look at the condo corporation’s reserve fund, the percentage of units that are owner-occupied vs. rented, and whether the building is on any lender’s “do not lend” list. Yes, those lists exist, and they’re more common than you’d think.

Mortgage rules change frequently, so what worked last year might not apply today — schedule a free strategy session with us to get current, personalized guidance.

What the Stress Test Means for Your Numbers

Most new investment property mortgages in Canada still go through the stress test. Your broker qualifies you at the higher of your actual mortgage rate plus 2% or 5.25% — whichever is greater. OSFI removed the stress test for non-insured renewals and straight lender switches in late 2024, but for purchases of new investment properties, the test still applies in full.

For investors, the stress test hits harder because you’re typically carrying other mortgages already. Each existing mortgage eats into your debt service ratios even if your rental income covers the payments. The stress test is applied at the higher qualifying rate, not your actual rate, which means the lender is testing whether you could handle payments if rates jumped significantly.

Here’s what that looks like in practice. Say you’re looking at a property with a $2,000/month mortgage payment at your actual rate. The stress test might bump that to $2,600/month for qualification purposes. Multiply that effect across three or four properties and you can see how the stress test creates a ceiling on how many properties you can hold through traditional residential lending.

Understanding this math before you start shopping prevents the disappointment of falling in love with a property you can’t finance.

Timeline: How Long Does Pre-Approval Take?

If your documents are organized and complete, a typical pre-approval timeline looks like this:

Day 1-2: Submit your application and all documents to your broker.

Day 2-3: Broker reviews everything, asks for any missing items, and submits to the lender.

Borrowers comparing options often continue with Organized Documents = Better Mortgage Rates (Here’s Why) before booking a strategy call.

Day 3-7: Lender reviews and issues the pre-approval (or asks for more documentation).

Total: 5-7 business days if everything goes smoothly.

But here’s the thing—“if everything goes smoothly” is doing a lot of heavy lifting in that sentence. In reality, most delays happen because:

- Documents are missing or incomplete

- Bank statements don’t cover the full 90 days

- Income documentation doesn’t match what was stated on the application

- There are unexplained large deposits that need sourcing

- The borrower has debts they forgot to mention

Every time the lender comes back with a question, add another 2-3 business days. I’ve seen pre-approvals that should have taken a week drag on for a month because the investor wasn’t prepared.

Do yourself a favor: get everything together before you contact your broker. It makes the whole process faster and smoother.

The Pre-Approval Process Step by Step

- Choose your mortgage professional — work with a broker experienced in investment properties, not just your retail bank.

- Initial consultation — review your financial situation, portfolio plans, and lender fit before formal application.

- Document submission — submit a complete package the first time to avoid back-and-forth delays.

- Credit pull and analysis — the lender verifies income, assets, and debt ratios.

- Pre-approval decision — you receive a letter with maximum amount, rate hold, and conditions (typically valid 90–120 days).

- Property-specific approval — once you find a deal, the lender appraises the property and issues final approval.

Strengthening Your Application

- Reduce revolving debt before applying — even small paydowns can improve TDS ratios.

- Increase your down payment beyond the 20% minimum when possible — it signals stability and may improve rates.

- Document rental income properly — signed leases, consistent deposits, and tax returns that match your stated income.

- Choose the right lender — investor-friendly lenders treat rental income and portfolio size differently. Explore investment property mortgage rates in Canada to understand what’s available.

Common Pre-Approval Challenges

Growing portfolio size. Most A lenders limit investors to four or five mortgages. Beyond that, alternative lenders or portfolio strategies may be required.

Self-employment income. Lower reported income for tax efficiency can hurt qualification. Some lenders offer stated-income programs for qualified borrowers.

Recent credit events. Bankruptcies, consumer proposals, or major delinquencies affect approval for years. Be transparent with your broker so they can match you to the right lender.

What to Do Before You Apply

There are several things you should handle before you even start the pre-approval process. Think of this as your pre-pre-approval checklist.

Check your credit score. You can get a free credit report from Equifax or TransUnion in Canada. For investment properties, most A lenders want to see a score of 680 or higher. Some B lenders will work with lower scores but at higher rates. If your score needs work, it’s better to know that now and fix it before applying.

Pay down revolving debt. Credit card balances and lines of credit directly impact your debt service ratios. Even paying down a few thousand dollars can improve your qualification. Focus on high-balance revolving accounts first.

Don’t open new credit. Every new credit application creates a hard inquiry on your report, which temporarily lowers your score. Don’t sign up for a new credit card, car loan, or furniture financing plan in the months before applying for your mortgage.

Don’t change jobs. Lenders like stability. If you’re planning a career move, try to do it well after your mortgage closes. Switching jobs during the process—especially to a new industry or from employed to self-employed—can derail your approval.

Save more than the minimum. You need 20% for the down payment, but you also need to cover closing costs (typically 1.5-4% of the purchase price), which include legal fees, land transfer tax, title insurance, and a property inspection. Our document checklist for investment property mortgages covers every item your lender will ask for. Having reserves beyond your down payment shows the lender you’re not stretching too thin.

Organize your rental documentation. If you already own rental properties, make sure your leases are current and your tax returns accurately reflect your rental income. Discrepancies between your stated rental income and your tax returns are a common reason for pre-approval delays.

The Pre-Approval Letter: What It Actually Means

Once approved, you’ll receive a pre-approval letter or certificate. Here’s what it does and doesn’t guarantee:

It does: Confirm that the lender has reviewed your financial profile and is willing to lend you up to a specific amount. It typically locks in an interest rate for 90-120 days.

It doesn’t: Guarantee you’ll get the mortgage. The lender still needs to approve the specific property you want to buy. They’ll order an appraisal, review the property’s condition and location, and confirm it meets their lending criteria. If the property doesn’t appraise at the purchase price or has issues the lender doesn’t like, the mortgage can still fall through.

This is why your pre-approval is the starting point, not the finish line. It gets you in the game, but you still need to pick properties that lenders will actually fund.

Your Action Plan

Here’s what I want you to do this week:

- Download your credit report and check your score.

- Make a list of every debt you owe, including balances and minimum payments.

- Gather every document on the checklist above.

- Put it all in one folder—digital is fine.

- Contact a mortgage broker who specializes in investment properties — or jump to our investor pre-approval hub to get started.

That’s it. Five steps, and you’re ahead of 90% of investors who wing it and waste time.

Getting pre-approved isn’t glamorous. Nobody posts about it on social media. But it’s the foundation that every successful property purchase is built on. When you are ready, apply for your mortgage to lock the right lender path — or use the strategy call CTA if you want a walkthrough first.

Key Takeaways:

- Pre-Approval vs. Pre-Qualification: Know the Difference

- The Document Checklist

- How Income Calculation Works for Investors

- Property Type Considerations

- What the Stress Test Means for Your Numbers

Frequently Asked Questions

How long does a mortgage pre-approval last?

Does getting pre-approved hurt my credit score?

Can I get pre-approved for an investment property if I already have a mortgage on my primary residence?

What credit score do I need for an investment property mortgage?

Can I use my RRSP for an investment property down payment?

Do I need a larger down payment if I already own multiple properties?

What if I can't provide two years of tax returns because I recently started a new job?

Should I get pre-approved before or after finding a property?

Does pre-approval guarantee I'll get the mortgage?

Can I get pre-approved for multiple properties at once?

Sources

Rates and program rules are subject to change. Verify current figures with primary sources:

- Bank of Canada — policy interest rate

- CMHC — multifamily and mortgage insurance programs

- OSFI — mortgage underwriting guidelines

Disclaimer: LendCity Mortgages is a licensed mortgage brokerage. Content on this page is for educational purposes only and does not constitute legal, tax, investment, securities, or financial-planning advice. Rates, premiums, program terms, and regulations referenced are as of the page's last updated date and are subject to change. Any investment returns, rental yields, tax savings, or case-study figures shown are illustrative only — they are not guaranteed, not typical, and individual results will vary. Consult a licensed lawyer, Chartered Professional Accountant, or registered dealer before acting on any information above. Editorial standards.

Written by

Scott Dillingham

Published

February 15, 2026

· Updated July 21, 2026Reading time

14 min read

Bank of Canada

Canada's central bank that sets the overnight lending rate, which influences prime rates and mortgage costs across the country. Rate decisions directly impact variable mortgage rates and overall borrowing costs for real estate investors.

Mortgage Stress Test

A federal requirement to qualify at the higher of your contract rate +2% or the benchmark rate (around 5.25%). For investors, rental income can be used to offset this calculation, though lenders typically only count 50-80% of expected rent.

Pre-Approval

A conditional commitment from a lender stating your borrowing capacity, valid for 90-120 days. For investors, getting pre-approved helps you move quickly on deals and shows sellers you're a serious buyer with financing in place.

Down Payment

The upfront cash payment when purchasing a property. For 1-4 unit investment properties, minimum 20% down is required. 5+ unit multifamily can use CMHC MLI Select with lower down payments, and house hackers can put as little as 5% down on owner-occupied 2-4 plexes. Your down payment directly affects your [LTV](/glossary/#ltv) and the amount of [leverage](/glossary/#leverage) you use.

CMHC Insurance

Mortgage default insurance from Canada Mortgage and Housing Corporation. For 1-4 unit investment properties, investors must put 20%+ down (no insurance available). However, CMHC offers MLI Select for 5+ unit multifamily properties, and house hackers can access insured mortgages with 5-10% down.

Private Mortgage

A mortgage from a private lender rather than a traditional bank, typically with higher rates but more flexible qualification requirements.

Commercial Lending

Financing for commercial real estate or business purposes, typically qualified based on property income (NOI) rather than personal income. Includes mortgages for multifamily buildings (5+ units), retail, office, and industrial properties.

Single Family

A detached home designed for one household, the most common property type for beginner real estate investors.

Closing Costs

Fees paid when completing a real estate transaction, including legal fees, land transfer tax, title insurance, appraisals, and adjustments. Closing costs affect your total cash invested and therefore your [cash-on-cash return](/glossary/#cash-on-cash-return).

Land Transfer Tax

A provincial tax paid when purchasing property, calculated as a percentage of the purchase price. Some cities like Toronto add additional municipal tax.

Credit Score

A numerical rating (300-900 in Canada) that represents your creditworthiness, affecting mortgage rates and approval. 680+ is typically needed for best rates.

Rental Offset

Using a percentage of rental income (typically 50-80%) to help qualify for a mortgage by offsetting property carrying costs.

Interest Rate

The cost of borrowing money, expressed as a percentage. It determines how much you pay on top of the principal borrowed. Interest rates directly affect monthly payments, [cash flow](/glossary/#cash-flow), and [DSCR](/glossary/#dscr). See also [Amortization](/glossary/#amortization).

Appraisal

A professional assessment of a property's market value, required by lenders to ensure the property is worth the loan amount.

Title Insurance

Insurance that protects against losses from defects in title to a property, such as liens, encumbrances, or ownership disputes.

Mortgage Broker

A licensed professional who shops multiple lenders to find the best mortgage rates and terms for borrowers. Unlike banks, brokers have access to dozens of lending options.

Rental Income

Revenue generated from tenants paying rent on an investment property. Gross rental income is the total collected before expenses, while net rental income subtracts operating costs to show actual profitability.

Property Inspection

A professional examination of a property's physical condition, including structural elements, mechanical systems, roofing, and other components, typically conducted before purchase. Thorough inspections help investors identify problems, estimate repair costs, and negotiate purchase prices.

Reserve Fund

Money set aside by a condo corporation or property owner for future major repairs and capital expenditures like roof replacement, building envelope repairs, or mechanical system upgrades. A well-funded reserve indicates responsible financial management and reduces the risk of special assessments.

Property Tax

Annual tax levied by municipalities on real estate based on the assessed value of the property. Property taxes fund local services and are a significant operating expense that investors must account for in cash flow projections.

Incorporation

The legal process of forming a corporation to own and operate investment properties. Incorporation creates a separate legal entity providing liability protection and tax planning options, but adds complexity and can affect mortgage qualification.

Rate Hold

A commitment from a lender to guarantee a specific mortgage interest rate for a set period, typically 90 to 120 days. Rate holds protect borrowers from increases while searching for a property or completing a purchase.

Condominium

A type of property ownership where an individual owns a specific unit within a larger building or complex, sharing ownership of common areas with other unit owners. Condos offer lower entry prices but come with monthly fees and potential rental restrictions that affect investment returns.

Strata Corporation

The governing body of a condominium building responsible for managing common property, collecting fees, maintaining reserve funds, and enforcing bylaws. The financial health of a strata corporation directly affects unit values and financing eligibility.

Foundation

The structural base of a building that transfers loads to the ground. Foundation issues such as cracks, settling, or water intrusion are among the most expensive repairs in real estate and can significantly impact property value and financing eligibility.

GDS

Gross Debt Service ratio - the percentage of gross income needed to cover housing costs (mortgage, taxes, heating). Maximum typically 39%. For investors, rental income from the property can offset these costs through rental offset calculations. See also [TDS](/glossary/#tds) and [Mortgage Stress Test](/glossary/#mortgage-stress-test).

TDS

Total Debt Service ratio - the percentage of gross income needed to cover all debt payments. Maximum typically 44%. Investors can use rental income (50-80% offset) to help qualify, making it possible to scale a portfolio despite existing debts. See also [GDS](/glossary/#gds) and [DSCR](/glossary/#dscr).

Debt Service Ratio

A broad term for ratios measuring a borrower's ability to service debt. In Canadian residential lending, the key ratios are GDS and TDS. In commercial lending, the DSCR serves a similar function but focuses on property income rather than personal income.

Notice of Assessment

A document issued by the CRA after processing a tax return, confirming income reported and taxes owed or refunded. Mortgage lenders require Notices of Assessment as proof of declared income, especially for self-employed borrowers.

Net Worth Statement

A financial document listing all assets and liabilities to calculate total net worth. Commercial and portfolio lenders often require this as part of mortgage applications, using total equity across all properties as a qualification factor.

Hover over terms to see definitions. View the full glossary for all terms.