Before you apply for a DSCR loan, you need to know exactly what lenders are looking for. Unlike conventional mortgages where your personal income drives the approval, DSCR loans evaluate a combination of property performance, borrower creditworthiness, and deal structure.

This guide covers every DSCR loan requirement you will encounter during the application process: credit scores, down payments, DSCR ratio thresholds, property eligibility, reserve requirements, and more. By the end, you will know precisely where you stand and what you need to prepare before reaching out to a lender. For step-by-step guidance on qualifying for DSCR mortgages based on property cash flow, read our complete guide.

For a broader overview of how DSCR loans work, visit our complete DSCR loan guide.

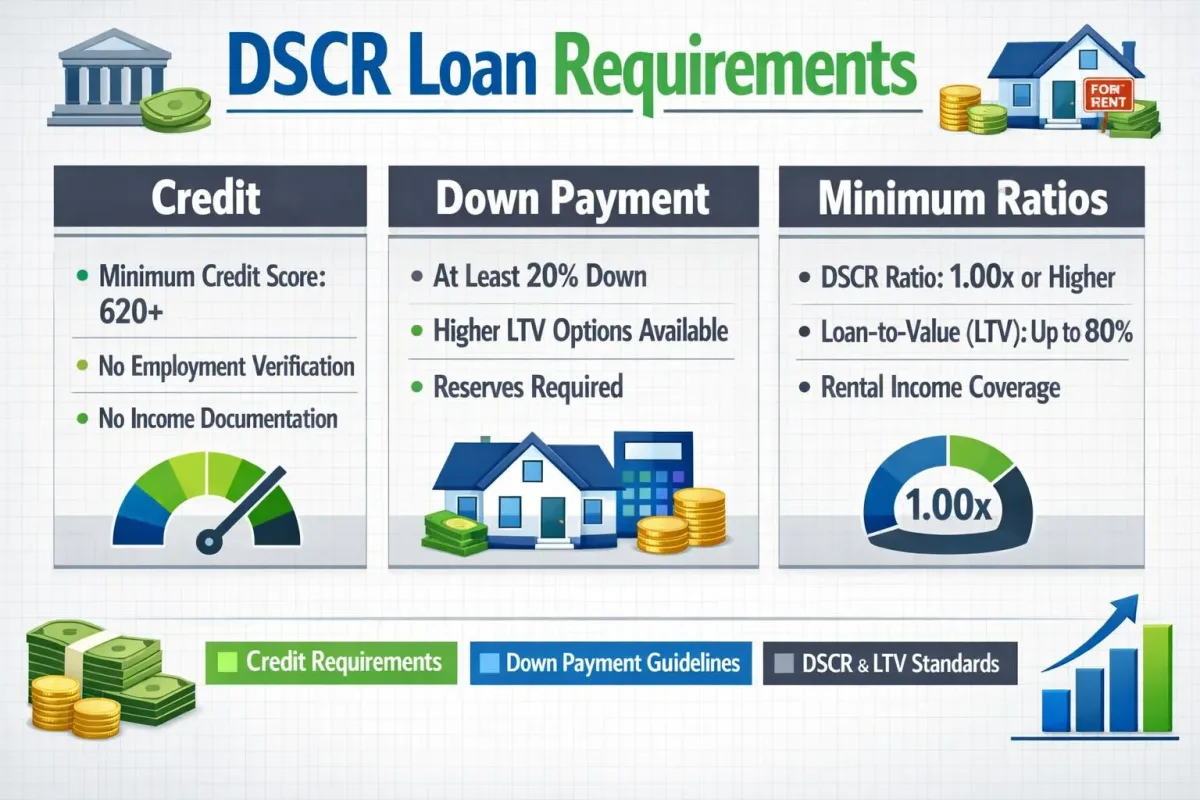

DSCR Ratio Requirements: The Core Qualification Metric

The debt service coverage ratio is the single most important number in your application. It measures whether the property’s rental income is sufficient to cover the mortgage payment.

Run your numbers through our DSCR Loan Calculator to see if your property qualifies.

DSCR = Gross Monthly Rent / PITIA (Principal + Interest + Taxes + Insurance + Association Dues)

Lenders use this ratio to tier their pricing and determine approval. Here is how the most common thresholds work:

DSCR of 1.25 or Higher

This is the sweet spot. A 1.25 DSCR means the property generates 25% more income than the mortgage payment requires. This level of coverage gives the lender strong confidence that the loan will perform, and it unlocks the best available rates and terms.

Example: If your PITIA is $2,000 per month, you need monthly rent of at least $2,500 to hit a 1.25 DSCR.

DSCR of 1.0 to 1.24

A DSCR in this range means the property covers the payment but with a thinner margin. Most lenders will still approve at this level, but you should expect modestly higher rates (typically 0.125% to 0.375% above the best tier) and potentially stricter requirements on other factors like credit score and down payment.

DSCR of 1.0 (Break-Even)

At exactly 1.0, the rent equals the mortgage payment. The property breaks even before accounting for maintenance, vacancies, and capital expenditures. Many lenders will approve at this level, though pricing will reflect the tighter margin. Some lenders treat 1.0 as their absolute minimum.

DSCR Below 1.0

Some lenders offer programs for properties with a DSCR as low as 0.75, meaning the rent covers only 75% of the mortgage payment. These “no-ratio” or “below 1.0” programs come with significant trade-offs: higher rates (often 1% to 2% above standard DSCR pricing), larger down payments (30% or more), and higher credit score requirements.

These programs exist for investors in high-appreciation markets where cash flow is secondary to equity growth, but they are not suitable for income-focused strategies.

| DSCR Range | Approval Likelihood | Rate Impact | Typical Down Payment |

|---|---|---|---|

| 1.25+ | Excellent | Best available rates | 20-25% |

| 1.10 - 1.24 | Strong | +0.125% to +0.25% | 20-25% |

| 1.0 - 1.09 | Good | +0.25% to +0.50% | 25% |

| 0.75 - 0.99 | Possible (select lenders) | +0.75% to +2.0% | 25-30% |

| Below 0.75 | Unlikely | N/A | N/A |

Credit Score Requirements

While DSCR loans do not verify your income, they absolutely check your credit. Your credit score is one of the primary factors that determines your interest rate, maximum loan-to-value ratio, and overall approval.

Minimum Credit Score Thresholds

For a side-by-side look at how rates, LTV caps, and reserve requirements shift across each band, the credit score tiers reference breaks down what to expect at each FICO level.

740 and above: This is the top tier. You will qualify for the best rates, the highest LTV options, and the most flexible terms. If your score is above 740, you are in an excellent position.

720 to 739: Still very strong. Most lenders offer near-best pricing at this level. You may see a slight rate bump of 0.125% compared to the 740+ tier, but terms remain favorable.

700 to 719: Solid qualification range. Rates will be modestly higher (0.25% to 0.375% above the top tier), and some lenders may cap your LTV at 75% instead of 80%.

680 to 699: This is where requirements start tightening. Expect rates that are 0.50% to 0.75% above the best available, and maximum LTV of 70% to 75% with many lenders. You will still have plenty of options, but the cost of borrowing increases noticeably.

660 to 679: The lower end of the qualifying range for most DSCR lenders. Rates will be significantly higher (1.0% or more above top-tier), and down payment requirements of 25% to 30% are common. Fewer lenders will work with this credit tier.

Below 660: Very few DSCR lenders will approve at this level. Those that do will charge premium rates and require substantial down payments (30% to 35%). If your score is below 660, it is worth investing time in credit improvement before applying.

What Credit Score Should You Target?

If you have time before applying, aim for 720 or higher. The rate savings between a 680 and a 740 credit score can be 0.75% to 1.25%, which on a $300,000 loan translates to $180 to $300 per month. Over a five-year hold, that is $10,800 to $18,000 in savings.

For detailed strategies on improving your rate, see our DSCR loan rates guide.

Before you commit to any mortgage product, it helps to get a second opinion — book a free strategy call with LendCity to see which options actually fit your financial picture.

Down Payment Requirements

The down payment (or equivalently, the loan-to-value ratio) is the second major factor in DSCR loan qualification. Here is what to expect:

Standard Down Payment Ranges

20% down (80% LTV): Available to borrowers with strong credit (720+), a DSCR of 1.25 or higher, and a property type that the lender is comfortable with (typically single-family or standard condo). This is the lowest down payment most DSCR lenders will offer.

25% down (75% LTV): The most common requirement for borrowers in the 680-720 credit range or for properties with a DSCR between 1.0 and 1.24. This is the baseline expectation for most DSCR transactions.

30% down (70% LTV): Required for lower credit scores (660-679), DSCR ratios below 1.0, non-warrantable condos, or other risk factors. Also common for cash-out refinances.

35% or more down: Rare, but may be required for properties with very low DSCR ratios, rural locations, or borrowers with recent credit events.

How to Reduce Your Down Payment

Several strategies can help you qualify for a lower down payment:

Improve your credit score. Moving from 700 to 740 can unlock 80% LTV instead of 75% LTV, reducing your cash requirement by tens of thousands of dollars.

Choose properties with strong rental income. A higher DSCR gives the lender more confidence and may qualify you for higher leverage.

Work with the right lender. Down payment requirements vary significantly between lenders. Some newer market entrants and portfolio lenders offer more aggressive LTV options to win business.

For an in-depth look at down payment strategies, read our DSCR loan down payment guide.

Reserve Requirements

Almost every DSCR lender requires you to have reserves (liquid assets) after closing. Reserves demonstrate that you can handle vacancies, repairs, or other unexpected expenses without defaulting on the loan. The full reserve requirements breakdown explains how lenders count retirement accounts, business funds, and gift money toward the post-closing reserve calculation.

Typical Reserve Amounts

3 to 6 months of PITIA: This is the standard range. If your monthly PITIA is $2,500, you need $7,500 to $15,000 in reserves after closing.

6 to 12 months of PITIA: Required for lower credit scores, lower DSCR ratios, or if you own a large number of investment properties. Some lenders also require reserves on your existing portfolio, not just the subject property.

What Counts as Reserves?

- Checking and savings accounts

- Money market accounts

- Stocks, bonds, and mutual funds (typically valued at 60% to 70% of market value)

- Retirement accounts like 401(k) and IRA (typically valued at 50% to 60%)

- Vested stock options

- Cash value of life insurance policies

Gift funds, borrowed money, and business accounts you do not control typically do not qualify as reserves.

Every borrower’s situation is different, and the wrong mortgage structure can cost you thousands — schedule a free strategy session with us to make sure you’re set up properly.

Property Type Eligibility

DSCR loans cover a broader range of property types than many investors realize, but there are limits.

Eligible Property Types

- Single-family residences (SFR): The most straightforward and widely accepted property type.

- 2-4 unit properties: Duplexes, triplexes, and fourplexes are eligible with most lenders.

- Warrantable condos: Standard condo units in HOA-approved buildings.

- Non-warrantable condos: Available with select lenders, often requiring a larger down payment.

- Townhomes: Generally treated similarly to single-family homes.

- 5-8 unit properties: Some DSCR lenders extend into this range, though terms may differ from 1-4 unit pricing.

- Short-term rentals: Many lenders accept Airbnb and VRBO properties, using AirDNA or actual booking data to calculate DSCR. Learn more about using DSCR loans to finance Airbnb and short-term rental properties.

Properties That Typically Do Not Qualify

- Vacant land

- Properties in non-rentable condition (major structural issues)

- Mobile homes or manufactured housing (some exceptions exist)

- Commercial properties (retail, office, industrial)

- Properties with more than 8 units (these fall under commercial financing)

- Agricultural properties

LLC and Entity Requirements

One of the most attractive features of DSCR loans is the ability to close in an LLC. Here is what lenders typically require:

Entity Structure

Most lenders accept single-member LLCs, multi-member LLCs, and corporations. The entity must be registered in the state where the property is located or have foreign entity authorization to do business in that state.

Personal Guarantee

Despite closing in an LLC, most DSCR lenders require a personal guarantee from the borrower (or the LLC’s managing member). This means you are personally liable for the debt if the LLC defaults. The guarantee is the reason the lender checks your personal credit score even though the loan is in the entity’s name.

Operating Agreement

Lenders will typically request a copy of the LLC’s operating agreement to verify ownership structure and management authority. If you are setting up a new LLC specifically for the purchase, have the operating agreement prepared before applying.

EIN Requirement

Your LLC will need an Employer Identification Number (EIN) from the IRS. This is free and can be obtained online in minutes. The EIN is used for the loan closing and any tax reporting.

Appraisal and Property Condition Requirements

Every DSCR loan requires a full appraisal. The appraisal serves two purposes: it establishes the property’s market value (which determines your LTV) and it confirms the property is in rentable condition.

Appraisal Standards

DSCR lenders use standard residential appraisals (Form 1004 or equivalent) for 1-4 unit properties. The appraisal includes comparable sales analysis, a rent survey or market rent analysis, and a condition assessment.

Rent Verification

The appraiser will include a rent analysis, but lenders may also use a separate rent schedule or third-party rental data (such as Rentometer or local MLS rental data) to determine the market rent used in the DSCR calculation. If the property is already occupied, the actual lease rent is typically used.

Property Condition

The property must be in move-in or rent-ready condition. Most DSCR lenders will not finance properties that need significant renovation. Common condition issues that can cause problems include:

- Peeling paint or damaged exteriors

- Roof at end of life

- Non-functional HVAC, plumbing, or electrical systems

- Foundation issues

- Health and safety hazards

If the property needs work, you may need to acquire it with a bridge or hard money loan, complete renovations, and then refinance into a DSCR loan once the property is stabilized.

Complete Requirements Summary Table

| Requirement | Standard | Notes |

|---|---|---|

| Minimum credit score | 660-680 | Best rates at 740+ |

| Down payment (purchase) | 20-25% | 30%+ for lower credit or low DSCR |

| Down payment (cash-out refi) | 25-30% | Some lenders allow 75% LTV |

| Minimum DSCR | 1.0 (most lenders) | Below 1.0 available with select lenders |

| Reserves | 3-6 months PITIA | Up to 12 months for larger portfolios |

| Property types | SFR, 2-4 unit, condo, townhome | 5-8 unit with select lenders |

| Loan amounts | $100,000 - $3,000,000+ | Minimums and maximums vary by lender |

| Loan terms | 30-year fixed, ARM options | Interest-only available |

| Entity closing | LLC, Corp accepted | Personal guarantee typically required |

| Seasoning (refinance) | 3-6 months | Some lenders require 6-12 months |

| Income documentation | Not required | Bank statements not needed |

| Property condition | Rent-ready | No major deferred maintenance |

How to Prepare Before Applying

Now that you know the requirements, here is a practical preparation checklist:

Step 1: Check your credit score. Pull your report from all three bureaus and dispute any errors. If your score is below 720, consider waiting and improving it before applying.

Step 2: Calculate the DSCR. Before making an offer on a property, estimate the DSCR using market rents and projected PITIA. If the ratio is below 1.0, either adjust your offer price or move on to a better deal.

Step 3: Prepare your reserves. Make sure you have enough liquid assets to cover both the down payment and the required reserves. Transfer funds to easily documented accounts at least 60 days before applying.

Step 4: Set up your LLC (if applicable). Register the entity, obtain an EIN, and draft the operating agreement. Having this done before you apply speeds up the process significantly.

Step 5: Gather property documents. If the property has existing leases, collect copies. If it is vacant, research comparable rents to support your DSCR calculation.

Step 6: Shop lenders. DSCR loan terms vary widely. Get quotes from at least three lenders and compare rates, fees, prepayment penalties, and reserve requirements. Our guide to understanding DSCR loan rates can help you evaluate offers.

To learn more about the full landscape of DSCR lending, including how it compares to other loan types, visit our what is a DSCR loan guide.

Key Takeaways:

- DSCR Ratio Requirements: The Core Qualification Metric

- Credit Score Requirements

- Down Payment Requirements

- Reserve Requirements

- Property Type Eligibility

Frequently Asked Questions

What is the minimum credit score for a DSCR loan?

How much do I need for a down payment on a DSCR loan?

Can I get a DSCR loan with a ratio below 1.0?

Do I need to show bank statements for a DSCR loan?

Can I use a DSCR loan for a short-term rental property?

How long does it take to close a DSCR loan?

What reserves do I need after closing on a DSCR loan?

Do I need an LLC to get a DSCR loan?

Next Steps

Understanding the requirements is the first step. The next step is finding the right lender, structuring your deal, and getting pre-qualified. Whether you are buying your first rental or adding to a growing portfolio, knowing exactly what lenders expect puts you ahead of the competition.

Sources

Rates and program rules are subject to change. Verify current figures with primary sources:

- Bank of Canada — policy interest rate

- CMHC — multifamily and mortgage insurance programs

- OSFI — mortgage underwriting guidelines

Disclaimer: LendCity Mortgages is a licensed mortgage brokerage. Content on this page is for educational purposes only and does not constitute legal, tax, investment, securities, or financial-planning advice. Rates, premiums, program terms, and regulations referenced are as of the page's last updated date and are subject to change. Any investment returns, rental yields, tax savings, or case-study figures shown are illustrative only — they are not guaranteed, not typical, and individual results will vary. Consult a licensed lawyer, Chartered Professional Accountant, or registered dealer before acting on any information above. Editorial standards.

Written by

Scott Dillingham

Published

February 15, 2026

· Updated June 9, 2026Reading time

13 min read

Down Payment

The upfront cash payment when purchasing a property. For 1-4 unit investment properties, minimum 20% down is required. 5+ unit multifamily can use CMHC MLI Select with lower down payments, and house hackers can put as little as 5% down on owner-occupied 2-4 plexes. Your down payment directly affects your [LTV](/glossary/#ltv) and the amount of [leverage](/glossary/#leverage) you use.

LTV

Loan-to-Value ratio - the mortgage amount expressed as a percentage of the property's appraised value or purchase price (whichever is lower). An 80% LTV means you're borrowing 80% and putting 20% [down](/glossary/#down-payment). Lower LTV generally means better [interest rates](/glossary/#interest-rate) and terms. See also [Equity](/glossary/#equity) and [Leverage](/glossary/#leverage).

DSCR

Debt Service Coverage Ratio — a metric that compares a property's [net operating income](/glossary/#noi) to its mortgage payments. A DSCR of 1.25 means the property generates 25% more income than needed to cover the debt. Lenders typically require a minimum DSCR of 1.0 to 1.25 for investment property loans (including [DSCR loans](/glossary/#dscr-loan)). See also [Cap Rate](/glossary/#cap-rate) and [Cash Flow](/glossary/#cash-flow).

Coverage Ratio

A measure of a property's ability to cover its debt payments, typically referring to DSCR. Commercial lenders often require a minimum of 1.2, meaning the property's net operating income exceeds debt payments by at least 20%.

Commercial Lending

Financing for commercial real estate or business purposes, typically qualified based on property income (NOI) rather than personal income. Includes mortgages for multifamily buildings (5+ units), retail, office, and industrial properties.

Cash Flow

The money left over after collecting rent and paying all expenses including mortgage, taxes, insurance, maintenance, and property management. Positive cash flow is the primary goal of buy-and-hold investors. See also [NOI](/glossary/#noi), [Cash-on-Cash Return](/glossary/#cash-on-cash-return), and [Vacancy Rate](/glossary/#vacancy-rate).

Appreciation

The increase in a property's value over time, which builds [equity](/glossary/#equity) and wealth for the owner through market growth or [forced improvements](/glossary/#forced-appreciation).

Equity

The difference between a property's current market value and the remaining mortgage balance. If your home is worth $500,000 and you owe $300,000, you have $200,000 in equity. Equity builds through mortgage payments, [appreciation](/glossary/#appreciation), and [forced appreciation](/glossary/#forced-appreciation). See also [LTV](/glossary/#ltv) and [Refinancing](/glossary/#refinancing).

Leverage

Using borrowed money (mortgage) to control a larger asset, amplifying both potential returns and risks on your investment. A higher [LTV](/glossary/#ltv) means more leverage. See also [Down Payment](/glossary/#down-payment) and [Equity](/glossary/#equity).

Single Family

A detached home designed for one household, the most common property type for beginner real estate investors.

Refinance

Replacing an existing mortgage with a new one, typically to access equity, get a better rate, or change terms. Investors commonly refinance to pull out capital for purchasing additional properties (cash-out refinance) while retaining ownership of the original property.

Cash-Out Refinance

Refinancing for more than you owe to pull out equity as cash, often used to fund down payments on additional investment properties.

DSCR Loan

A loan qualified based on the property's [Debt Service Coverage Ratio](/glossary/#dscr) rather than the borrower's personal income, popular for US investment properties. The property's [NOI](/glossary/#noi) and [cash flow](/glossary/#cash-flow) determine qualification.

LLC

Limited Liability Company — a US business structure commonly used to hold US investment properties. Important caveat for Canadian residents: the CRA generally treats a US LLC as a corporation for Canadian tax purposes, which can create mismatched treatment with the IRS and double taxation; many cross-border advisors recommend a US LP (with an LLC as general partner) or direct ownership instead. Entity choice is a legal and tax decision — consult a cross-border attorney and a CPA experienced in Canada–US tax before forming one.

Credit Score

A numerical rating (300-900 in Canada) that represents your creditworthiness, affecting mortgage rates and approval. 680+ is typically needed for best rates.

Interest Rate

The cost of borrowing money, expressed as a percentage. It determines how much you pay on top of the principal borrowed. Interest rates directly affect monthly payments, [cash flow](/glossary/#cash-flow), and [DSCR](/glossary/#dscr). See also [Amortization](/glossary/#amortization).

Principal

The original amount of money borrowed on a mortgage, not including interest. Each mortgage payment includes both principal (paying down what you owe) and interest (the cost of borrowing). Over time, more of each payment goes toward principal as the loan balance decreases.

Appraisal

A professional assessment of a property's market value, required by lenders to ensure the property is worth the loan amount.

Market Value

The estimated price a property would sell for on the open market under normal conditions. Determined by comparable sales, location, condition, and market demand.

Market Rent

The rental rate that a property could reasonably command in the current market based on comparable properties, location, and condition. Understanding market rent is essential to maximize income while maintaining competitive positioning and minimizing vacancy.

Rental Income

Revenue generated from tenants paying rent on an investment property. Gross rental income is the total collected before expenses, while net rental income subtracts operating costs to show actual profitability.

HVAC

Heating, Ventilation, and Air Conditioning systems that control temperature and air quality in buildings. HVAC is often one of the largest energy expenses in rental properties, and upgrading to high-efficiency systems can significantly reduce operating costs and increase NOI.

Deferred Maintenance

Necessary repairs and maintenance that have been postponed or neglected, creating a backlog of work that will eventually require attention. Properties with significant deferred maintenance can be value-add opportunities for investors willing to address accumulated issues.

Capital Expenditures

Major one-time expenses for property improvements that extend the useful life of the asset, such as roof replacement, foundation repairs, or new HVAC systems. CapEx differs from regular maintenance and is typically budgeted separately in investment property analysis.

Comparable Properties

Similar properties in the same market area used to establish fair market value or rental rates through comparison of features, location, condition, and recent sale or rental prices. Analyzing comps is essential when determining offer prices and setting competitive rents.

A Lender

A major bank or institutional lender offering the most competitive mortgage rates and terms but with the strictest qualification criteria, including full income verification and stress test compliance. Most investors use A lenders for their first four to six properties.

Recourse Loan

A loan where the borrower is personally liable for repayment beyond the collateral value. If the property sells for less than owed at foreclosure, the lender can pursue the borrower's other assets. Most Canadian commercial mortgages under $5 million are full recourse.

Short-Term Rental

A furnished property rented for periods shorter than 30 days through platforms like Airbnb or VRBO. Short-term rentals generate higher gross revenue but carry higher operating costs and stricter municipal regulations.

Airbnb

An online marketplace connecting property owners with short-term guests. In real estate investing, Airbnb is commonly used as shorthand for the short-term rental business model, which involves higher operational demands but potentially higher returns than long-term rentals.

Condominium

A type of property ownership where an individual owns a specific unit within a larger building or complex, sharing ownership of common areas with other unit owners. Condos offer lower entry prices but come with monthly fees and potential rental restrictions that affect investment returns.

Townhouse

A multi-story residential unit that shares one or more walls with adjacent units but has its own entrance. Townhouses offer a middle ground between condos and detached homes, often with lower purchase prices and condo-like fee structures.

Raw Land

Undeveloped property without buildings, utilities, or infrastructure. Raw land investments offer potential for development or appreciation but generate no rental income and can be difficult to finance through traditional lenders.

MLS

Multiple Listing Service - a database used by licensed real estate agents to list properties for sale, providing standardized property information, photos, and pricing. Investors also use off-market strategies to find deals not listed on the MLS.

Hard Money Loan

A short-term loan from private lenders secured by the property itself rather than the borrower's creditworthiness. Hard money loans offer fast approvals and flexible terms but at higher interest rates, commonly used for fix-and-flip projects and bridge financing.

Cash Reserve

Liquid funds set aside by a property investor to cover unexpected expenses such as repairs, vacancy periods, or mortgage payments during tenant turnover. Lenders may require proof of cash reserves as part of mortgage qualification.

Plumbing

The system of pipes, drains, fixtures, and fittings in a building that distributes water and removes waste. Plumbing issues are among the most costly repairs in rental properties, and older galvanized or polybutylene pipes often need replacement during renovations.

Foundation

The structural base of a building that transfers loads to the ground. Foundation issues such as cracks, settling, or water intrusion are among the most expensive repairs in real estate and can significantly impact property value and financing eligibility.

Hover over terms to see definitions. View the full glossary for all terms.