You’ve found the property, your offer was accepted, and your DSCR loan financing is moving forward. Now comes the part that makes most first-time investors nervous: closing. The DSCR loan closing process involves multiple parties, specific timelines, and costs that you need to understand before you get to the finish line.

Here’s exactly what happens between going under contract and getting the keys, so nothing catches you off guard.

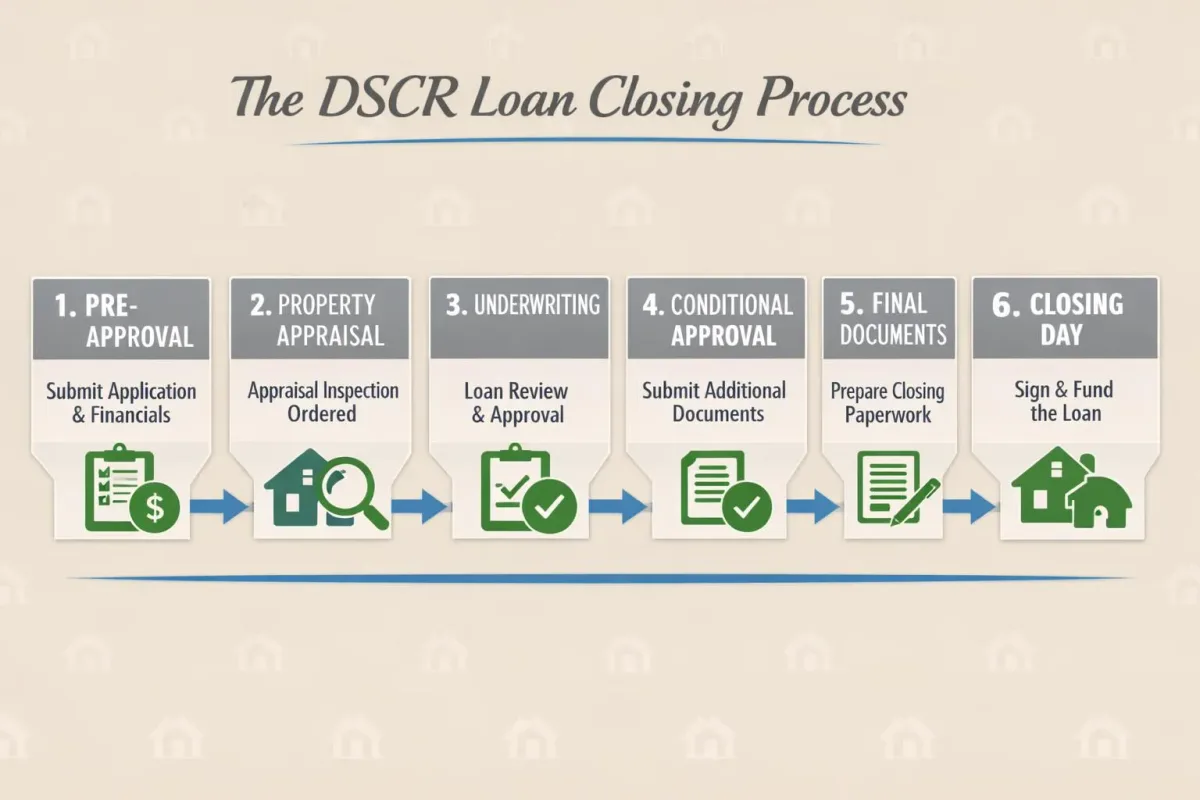

Overall Closing Timeline

A typical DSCR loan closes in 21 to 45 days from the time you go under contract. The most common timeline is around 30 days, but several factors affect your speed:

- Property type: Single-family homes close faster than multifamily properties

- Appraisal turnaround: This is usually the biggest variable, ranging from 5 to 14 days depending on the market

- Title search complexity: Clean title histories close quickly; properties with liens or encumbrances take longer

- Your responsiveness: How fast you return signed documents and satisfy conditions directly impacts your timeline

If you got pre-approved for your DSCR loan before finding the property, you’ve already shaved 5 to 10 days off this timeline since your borrower profile is already verified. For a milestone-by-milestone view of where each day goes, this DSCR loan process timeline maps every step from application to funding.

Run your numbers through our DSCR loan calculator tool to see if your property qualifies.

Phase-by-Phase Breakdown

Phase 1: Application and Document Submission (Days 1-3)

Once you’re under contract, you formally submit your loan application along with the purchase contract and property details. If you’re already pre-approved, this phase is mostly about providing the specific property information to your lender. For a full walkthrough of the application itself, see our guide on how to apply for a DSCR loan.

Your lender will need:

- Fully executed purchase agreement

- Property address and legal description

- Expected rental income documentation (existing leases or market rent analysis)

- Proof of earnest money deposit

- Updated bank statements (if more than 30 days old from pre-approval)

Phase 2: Appraisal Ordering (Days 3-7)

The lender orders a property appraisal from a licensed, independent appraiser. This is one of the most critical steps in a DSCR loan because the appraiser determines two things:

- Fair market value of the property (which affects your loan-to-value ratio)

- Market rent analysis (which determines your DSCR ratio)

The appraisal typically costs $400 to $800 for a single-family property and $800 to $1,500 for a small multifamily. You pay this upfront, and it’s non-refundable even if the deal falls through.

Appraisal turnaround varies by market. In busy metros like Phoenix or Atlanta, expect 7 to 14 days. In smaller markets, you might get it back in 5 to 7 days.

What can go wrong: The appraised value comes in lower than the purchase price, reducing your loan amount. Or the market rent analysis shows rents too low to meet the minimum DSCR ratio (typically 1.0 to 1.25). Either scenario requires renegotiation with the seller or bringing more cash to closing.

Phase 3: Title Search and Insurance (Days 3-10)

Running in parallel with the appraisal, the title company conducts a thorough search of the property’s ownership history. They’re looking for:

- Outstanding liens (tax liens, mechanic’s liens, judgment liens)

- Easements or encroachments

- Unresolved ownership claims

- HOA violations or unpaid assessments

- Any defects in the chain of title

Once the title search comes back clean, the title company issues a title commitment, which is essentially a promise to insure the property’s title at closing. You’ll purchase a lender’s title insurance policy (required) and optionally an owner’s title insurance policy (strongly recommended).

Lender’s title insurance protects the lender’s interest in the property. Cost is typically $500 to $1,500 depending on the loan amount and state.

Owner’s title insurance protects your equity. It’s a one-time fee at closing, usually $500 to $2,000. Skip this at your own risk. A title defect discovered years later could cost you the entire property.

Phase 4: Insurance Binding (Days 5-15)

You need to secure property insurance (hazard insurance) before closing. The lender requires proof that the property is insured for at least the loan amount. You’ll need:

- Hazard/property insurance covering fire, wind, and other covered perils

- Flood insurance if the property is in a FEMA-designated flood zone

- Liability insurance (typically included in your property insurance policy)

For a single-family rental, expect to pay $1,200 to $3,000 annually for property insurance, depending on the location, property value, and coverage amounts. Flood insurance, if required, adds $500 to $3,000+ annually.

Get quotes from at least three insurance providers. Your insurance agent needs to list the lender as a mortgagee on the policy and provide a binder (proof of insurance) to the title company before closing.

Phase 5: Underwriting Conditions (Days 10-25)

This is where underwriting digs into every detail. After receiving the appraisal, title commitment, and insurance binder, the underwriter reviews everything and issues a list of conditions that must be cleared before the loan can close.

Common DSCR loan underwriting conditions include:

- Verification of reserves (updated bank statements showing sufficient funds for down payment, closing costs, and required reserves)

- Entity verification (confirmation your LLC is in good standing)

- Lease review (if existing tenants, the underwriter reviews current lease agreements)

- Insurance confirmation (proper coverage amounts and mortgagee clause)

- Appraisal clarifications (sometimes the underwriter asks the appraiser follow-up questions about comparable properties or condition ratings)

- Property condition requirements (if the appraiser noted deferred maintenance, the underwriter may require repairs before closing)

Respond to conditions quickly. Every day you delay extends your closing timeline. The best practice is to respond to all conditions within 24 to 48 hours.

Phase 6: Clear to Close (Days 20-35)

Once all underwriting conditions are satisfied, you receive the magic words: clear to close (CTC). This means the loan is fully approved and the lender is ready to fund.

At this point, the closing team (typically the title company or closing attorney, depending on the state) prepares the closing documents. This includes the mortgage note, deed of trust, settlement statement, and all required disclosures.

For a deeper look at the financing angle behind this topic, see our guide to DSCR Loan Financing.

Phase 7: Closing Disclosure (3 Business Days Before Closing)

Federal law requires that you receive a Closing Disclosure (CD) at least three business days before your closing date. This document details every cost, credit, and adjustment in the transaction.

Review the CD carefully and compare it to the Loan Estimate you received at the beginning of the process. Key items to verify:

- Loan amount and interest rate match what was agreed upon

- Monthly payment breakdown (principal, interest, taxes, insurance)

- All closing costs are accurately reflected

- Prepayment penalty terms (if applicable)

- Cash due at closing matches your expectations

If there are material changes to the CD after it’s issued, the three-day clock resets, which can delay your closing.

Phase 8: Closing Day (Signing)

On closing day, you sign the final documents. Depending on your state and situation, this can happen in person at the title company or remotely.

In-person closing: You sit down with a closing agent at the title company or attorney’s office. Plan for 45 minutes to an hour of signing.

Remote closing / e-signing: Many states now allow remote online notarization (RON), which lets you sign everything digitally via video call. This is especially useful for out-of-state investors. Your lender and title company can confirm whether your state and county support RON closings.

Power of attorney: If you can’t attend in person and RON isn’t available, you can sometimes grant power of attorney to a trusted representative to sign on your behalf. This requires advance coordination with the lender and title company.

Phase 9: Funding and Recording (1-3 Days After Signing)

After all documents are signed, the lender wires the loan proceeds to the title company. The title company disburses funds to the seller, pays off any existing liens, distributes closing costs, and records the deed and mortgage with the county.

In some states (known as “table funding” states), funding happens simultaneously with signing. In others, there’s a 24 to 72-hour gap between signing and funding.

You officially own the property once the deed is recorded with the county. The title company will send you a copy of the recorded deed, which may take a few weeks to arrive.

Choosing the wrong lender or term can quietly erode your returns — book a free strategy call with LendCity and we’ll walk you through the numbers.

Typical Closing Costs Breakdown

DSCR loan closing costs typically run 2% to 5% of the loan amount. On a $250,000 loan, expect $5,000 to $12,500 in total closing costs. For a deeper itemization of every line you might see, this guide to closing costs and fees on DSCR loans explains which charges are negotiable and which are fixed by the lender or state. Here’s how that breaks down:

Lender Fees

| Fee | Typical Cost |

|---|---|

| Origination fee (1-2 points) | $2,500 - $5,000 |

| Underwriting fee | $500 - $1,000 |

| Processing fee | $300 - $750 |

| Credit report | $50 - $100 |

| Flood certification | $15 - $25 |

Third-Party Fees

| Fee | Typical Cost |

|---|---|

| Appraisal | $400 - $1,500 |

| Title search | $200 - $500 |

| Lender’s title insurance | $500 - $1,500 |

| Owner’s title insurance | $500 - $2,000 |

| Closing/settlement fee | $300 - $800 |

| Recording fees | $100 - $300 |

| Survey (if required) | $300 - $600 |

Prepaid Items and Escrow

| Item | Typical Cost |

|---|---|

| Prepaid interest (per diem x days to month end) | $200 - $1,000 |

| Property insurance (first year) | $1,200 - $3,000 |

| Property tax escrow (2-4 months) | $500 - $2,000 |

| Insurance escrow (2-3 months) | $200 - $750 |

Real Example

For a $300,000 purchase with a $225,000 DSCR loan (25% down), here’s what realistic closing costs look like:

- Origination (1.5 points): $3,375

- Underwriting fee: $750

- Processing fee: $500

- Appraisal: $550

- Title search and insurance: $1,800

- Closing fee: $500

- Recording: $175

- Prepaid interest (15 days): $575

- Property insurance (year 1): $2,100

- Tax escrow (3 months): $1,125

- Insurance escrow (2 months): $350

Total closing costs: approximately $11,800

Combined with the $75,000 down payment, total cash needed at closing is approximately $86,800. For a full breakdown of what lenders expect, see our DSCR loan down payment guide.

Closing in an LLC Name

Most DSCR loans close in the name of your LLC, not your personal name. This adds a few requirements:

- Your LLC must be in good standing with the state where it’s registered

- The Operating Agreement must authorize the signing member to execute loan documents

- The title and insurance must be in the LLC’s name

- Your LLC’s EIN is used for all closing documents

If your LLC is registered in a different state than the property, you may need to register as a foreign entity in the property’s state. Check with your attorney or CPA before closing.

Your debt ratios, income type, and property plans all affect what you qualify for — schedule a free strategy session with us so we can map out a strategy that works for your goals.

Wire Fraud Warning

Wire fraud is one of the biggest threats in real estate transactions today. Criminals hack email accounts and send fake wiring instructions that look legitimate. Here’s how to protect yourself:

- Never trust wiring instructions received by email alone. Always call the title company directly using a phone number you independently verify (from their website, not from the email) to confirm wire details.

- Verify the account number, routing number, and beneficiary name on a live phone call before sending any funds.

- Send a small test wire first ($100) and confirm receipt before wiring the full amount.

- Be suspicious of any last-minute changes to wiring instructions. This is the most common fraud tactic.

If you wire funds to the wrong account, recovery is extremely difficult and often impossible. Take the extra 10 minutes to verify everything.

What to Bring to Closing

If closing in person, bring:

- Government-issued photo ID (driver’s license or passport)

- Cashier’s check or wire confirmation for the amount due at closing (personal checks are almost never accepted for large sums)

- A copy of your LLC documents (Articles of Organization, Operating Agreement, EIN letter)

- Proof of insurance (your insurance agent should have already sent this to the title company, but bring a copy just in case)

Post-Closing Expectations

After closing, here’s what happens next:

Within 1-2 weeks: You receive copies of all recorded documents from the title company, including the deed and mortgage.

Within 30 days: Your loan may be sold or transferred to a servicing company. You’ll receive a notice from both the original lender and the new servicer. This is completely normal and doesn’t change your loan terms.

Within 45-60 days: You receive your final title insurance policy from the title company.

Ongoing: Set up your mortgage payment with the loan servicer. Most DSCR loans offer auto-debit options. Make sure your first payment goes to the right servicer, especially if the loan was transferred.

If the property came with existing tenants, coordinate with the previous owner for a smooth handoff of security deposits, lease agreements, and tenant communications. If it’s vacant, start your tenant placement process right away to begin generating the rental income your DSCR ratio depends on.

For tips on avoiding problems throughout this entire financing journey, check out our guide on DSCR loan mistakes to avoid.

Key Takeaways:

- Overall Closing Timeline

- Phase-by-Phase Breakdown

- Typical Closing Costs Breakdown

- Closing in an LLC Name

- Wire Fraud Warning

Frequently Asked Questions

How long does it take to close a DSCR loan?

What are typical closing costs on a DSCR loan?

Can I close a DSCR loan remotely without being physically present?

Can I close a DSCR loan in my LLC's name?

What happens if the appraisal comes in low on a DSCR loan?

Do I need to set up an escrow account for taxes and insurance?

What is the Closing Disclosure and when do I receive it?

How do I protect myself from wire fraud during closing?

Disclaimer: LendCity Mortgages is a licensed mortgage brokerage. Content on this page is for educational purposes only and does not constitute legal, tax, investment, securities, or financial-planning advice. Rates, premiums, program terms, and regulations referenced are as of the page's last updated date and are subject to change. Any investment returns, rental yields, tax savings, or case-study figures shown are illustrative only — they are not guaranteed, not typical, and individual results will vary. Consult a licensed lawyer, Chartered Professional Accountant, or registered dealer before acting on any information above. Editorial standards.

Written by

Scott Dillingham

Published

February 15, 2026

· Updated June 29, 2026Reading time

13 min read

Pre-Approval

A conditional commitment from a lender stating your borrowing capacity, valid for 90-120 days. For investors, getting pre-approved helps you move quickly on deals and shows sellers you're a serious buyer with financing in place.

Down Payment

The upfront cash payment when purchasing a property. For 1-4 unit investment properties, minimum 20% down is required. 5+ unit multifamily can use CMHC MLI Select with lower down payments, and house hackers can put as little as 5% down on owner-occupied 2-4 plexes. Your down payment directly affects your [LTV](/glossary/#ltv) and the amount of [leverage](/glossary/#leverage) you use.

LTV

Loan-to-Value ratio - the mortgage amount expressed as a percentage of the property's appraised value or purchase price (whichever is lower). An 80% LTV means you're borrowing 80% and putting 20% [down](/glossary/#down-payment). Lower LTV generally means better [interest rates](/glossary/#interest-rate) and terms. See also [Equity](/glossary/#equity) and [Leverage](/glossary/#leverage).

DSCR

Debt Service Coverage Ratio — a metric that compares a property's [net operating income](/glossary/#noi) to its mortgage payments. A DSCR of 1.25 means the property generates 25% more income than needed to cover the debt. Lenders typically require a minimum DSCR of 1.0 to 1.25 for investment property loans (including [DSCR loans](/glossary/#dscr-loan)). See also [Cap Rate](/glossary/#cap-rate) and [Cash Flow](/glossary/#cash-flow).

Equity

The difference between a property's current market value and the remaining mortgage balance. If your home is worth $500,000 and you owe $300,000, you have $200,000 in equity. Equity builds through mortgage payments, [appreciation](/glossary/#appreciation), and [forced appreciation](/glossary/#forced-appreciation). See also [LTV](/glossary/#ltv) and [Refinancing](/glossary/#refinancing).

Multifamily

Properties with multiple dwelling units, from duplexes to large apartment buildings. Often offer better cash flow and economies of scale.

Single Family

A detached home designed for one household, the most common property type for beginner real estate investors.

DSCR Loan

A loan qualified based on the property's [Debt Service Coverage Ratio](/glossary/#dscr) rather than the borrower's personal income, popular for US investment properties. The property's [NOI](/glossary/#noi) and [cash flow](/glossary/#cash-flow) determine qualification.

LLC

Limited Liability Company — a US business structure commonly used to hold US investment properties. Important caveat for Canadian residents: the CRA generally treats a US LLC as a corporation for Canadian tax purposes, which can create mismatched treatment with the IRS and double taxation; many cross-border advisors recommend a US LP (with an LLC as general partner) or direct ownership instead. Entity choice is a legal and tax decision — consult a cross-border attorney and a CPA experienced in Canada–US tax before forming one.

Closing Costs

Fees paid when completing a real estate transaction, including legal fees, land transfer tax, title insurance, appraisals, and adjustments. Closing costs affect your total cash invested and therefore your [cash-on-cash return](/glossary/#cash-on-cash-return).

Mortgage Penalty

A fee charged for breaking your mortgage early, calculated as either 3 months' interest or the Interest Rate Differential (IRD), whichever is greater.

Interest Rate

The cost of borrowing money, expressed as a percentage. It determines how much you pay on top of the principal borrowed. Interest rates directly affect monthly payments, [cash flow](/glossary/#cash-flow), and [DSCR](/glossary/#dscr). See also [Amortization](/glossary/#amortization).

Principal

The original amount of money borrowed on a mortgage, not including interest. Each mortgage payment includes both principal (paying down what you owe) and interest (the cost of borrowing). Over time, more of each payment goes toward principal as the loan balance decreases.

Appraisal

A professional assessment of a property's market value, required by lenders to ensure the property is worth the loan amount.

Title Insurance

Insurance that protects against losses from defects in title to a property, such as liens, encumbrances, or ownership disputes.

Market Value

The estimated price a property would sell for on the open market under normal conditions. Determined by comparable sales, location, condition, and market demand.

Underwriting

The process lenders use to evaluate the risk of a mortgage application, including reviewing credit, income, assets, and property value to determine loan approval.

Market Rent

The rental rate that a property could reasonably command in the current market based on comparable properties, location, and condition. Understanding market rent is essential to maximize income while maintaining competitive positioning and minimizing vacancy.

Rental Income

Revenue generated from tenants paying rent on an investment property. Gross rental income is the total collected before expenses, while net rental income subtracts operating costs to show actual profitability.

Deferred Maintenance

Necessary repairs and maintenance that have been postponed or neglected, creating a backlog of work that will eventually require attention. Properties with significant deferred maintenance can be value-add opportunities for investors willing to address accumulated issues.

Property Tax

Annual tax levied by municipalities on real estate based on the assessed value of the property. Property taxes fund local services and are a significant operating expense that investors must account for in cash flow projections.

Comparable Properties

Similar properties in the same market area used to establish fair market value or rental rates through comparison of features, location, condition, and recent sale or rental prices. Analyzing comps is essential when determining offer prices and setting competitive rents.

A Lender

A major bank or institutional lender offering the most competitive mortgage rates and terms but with the strictest qualification criteria, including full income verification and stress test compliance. Most investors use A lenders for their first four to six properties.

Earnest Money

A deposit made by a buyer to demonstrate serious intent to purchase a property. In wholesaling, earnest money secures the purchase contract. If the deal falls through due to buyer default, the earnest money may be forfeited.

Hover over terms to see definitions. View the full glossary for all terms.