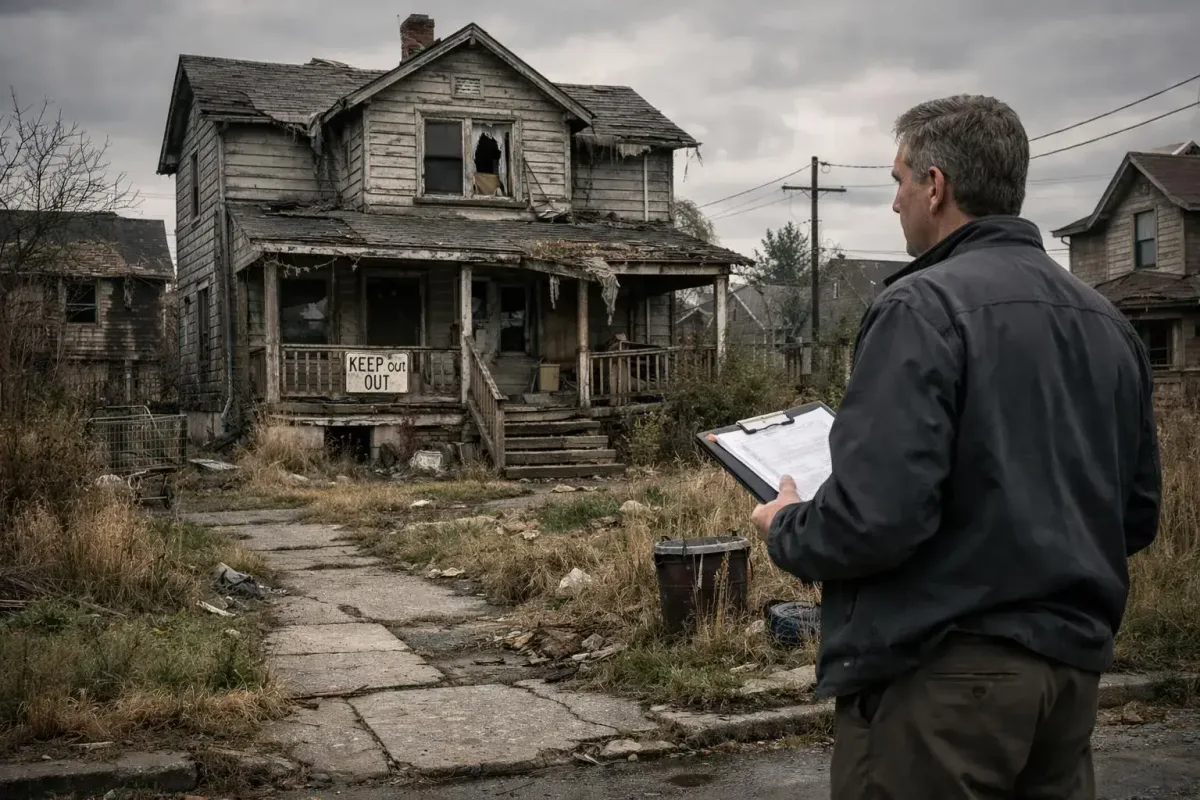

Every investor knows someone who bought a “great deal” that turned into a nightmare.

The property looked perfect. Good price. Nice location. Tons of potential. Then the problems started. And never stopped.

I’ve seen investors pour $80,000 into a house they bought for $40,000 under market value—and still not have a rentable property. That’s not a discount. That’s a trap.

Money pit properties don’t just drain your bank account. They steal your time, your sanity, and your opportunity to invest in properties that actually perform. The worst part? Most investors see the warning signs and ignore them because they’re excited about the “opportunity.”

Here’s how to spot these traps before they trap you.

What Actually Makes a Property a Money Pit?

Let’s be clear: a money pit isn’t just a property that needs work.

Every property needs repairs eventually. That’s real estate.

A money pit is a property where the costs never stop, the problems compound, and the returns never show up. It’s a property that requires so much spending that profitability becomes impossible—no matter how much you invest.

Properties turn into money pits through:

- Deferred maintenance that runs deeper than the surface

- Structural problems requiring major remediation (think $50,000+ foundation repairs)

- Environmental contamination—mold behind walls, asbestos in old insulation, lead paint, soil issues

- Location problems that permanently cap your income potential

- Hidden issues that sophisticated sellers know how to conceal

And the financial damage goes beyond repair invoices. You’ve got extended vacancy while you fix things. Carrying costs eating into your reserves. Opportunity costs from having your capital stuck in a non-performing asset while other investors snap up good deals.

Here’s a quick reference:

| Warning Sign | Why It Matters | How to Investigate |

|---|---|---|

| Priced 15%+ below market | Likely hiding problems | Pull comparable sales data |

| 90+ days on market | Buyers found issues | Ask for showing feedback |

| Visible deferred maintenance | Surface problems signal deeper ones | Get thorough inspection |

| Seller won’t negotiate on inspections | They know what inspectors will find | Walk away |

| Multiple owners in 5 years | People keep bailing | Pull title history |

Check the Neighbourhood First—Before the Property

Here’s a mistake I see constantly: investors fall in love with a property before researching the area.

Don’t do that.

A beautifully renovated house in a declining neighbourhood will never hit the values you need for profitable investing, no matter how much you spend on bathroom upgrades that increase rent or kitchen remodels. Learn how to find good real estate opportunities in Canadian markets before committing your capital. Meanwhile, a modest property in an improving area often exceeds expectations.

Do your homework on the location:

- Pull crime statistics from the local police service (most Canadian municipalities publish these)

- Check property value trends over the past 3-5 years on HouseSigma or Redfin

- Research school rankings—even if you’re renting to childless tenants, school quality drives neighbourhood demand

- Look for signs of improvement: new businesses, infrastructure investment, young families moving in

- Look for signs of decline: boarded storefronts, increasing crime, properties sitting unsold

If property values in an area are dropping while the rest of the market rises, that’s a fundamental problem you can’t renovate your way out of. Don’t buy hoping for neighbourhood turnaround unless you have concrete evidence—new transit line under construction, major employer moving in, rezoning approval—that change is actually happening.

Before you chase a property priced 15 percent below comparable sales, book a free strategy call with LendCity and we will help you figure out whether the discount covers the real repair costs or hides something worse.

Cash flow projections mean nothing if your mortgage eats into your returns — book a free strategy call with LendCity to make sure your financing supports your investment thesis.

The right financing product can change the math on this entirely — explore our real estate investing guide for the options most investors use.

What That Below-Market Price Really Means

When a property is priced 15% or more below comparable sales, your first question should be: why?

Sometimes sellers underprice because they need out fast. Divorce. Estate sale. Job relocation. These are legitimate reasons.

More often? That low price exists because sophisticated buyers have already walked away after discovering what’s wrong. Be sure to understand the common issues when buying distressed properties before jumping in.

Here’s how to decode pricing:

- Pull recent comparable sales within a 1 km radius (same neighbourhood, similar age and size)

- If the property is discounted more than 10-15%, dig deeper

- Calculate whether your purchase savings actually exceed the likely repair costs

- Ask the listing agent directly: “Why is this priced where it is?”

- Get rental property mortgage financing lined up so you can move quickly on properties that pass inspection

That “amazing deal” at $425,000 when similar homes sell for $500,000? There’s probably $100,000+ in problems waiting for you. You don’t want to be the investor who didn’t do the homework other buyers did.

Days on Market Tells a Story

When a property sits on the market for 60, 90, 120+ days in a market where similar homes sell in weeks, something’s wrong.

Properties don’t just sit. Buyers have discovered issues. Offers have fallen through. Inspections have revealed problems significant enough to kill deals.

Ask these questions:

For a deeper look at the financing angle behind this topic, see our guide to How to Spot a Money Pit: Telltale Signs of a Bad Investment Property.

- “How long has this been listed?”

- “Have there been other offers? What happened?”

- “Were there previous inspections? Can I see them?”

- “Has the price been reduced? Why?”

Listen carefully to how agents respond. They won’t volunteer negative information—but evasive answers tell you plenty. “The sellers are just being patient” after 120 days on market? That’s code for “every serious buyer has walked.”

If a property has been sitting on the market for 90-plus days and you still think the numbers work, book a free strategy call with us so we can stress-test the deal before you commit.

Getting your financing strategy right from the start saves you from costly mistakes down the road — schedule a free strategy session with us before you make your next move.

Professional Inspections Are Non-Negotiable

I’ll say this as directly as I can: never skip the inspection.

The cost—typically $400-$600 for a thorough inspection in most Canadian markets—is nothing compared to discovering major issues after you own the property. Yet investors skip inspections all the time. Competitive market. “Trusted their gut.” Wanted to make the offer more attractive.

Every one of those investors has a horror story.

Here’s how to do inspections right:

- Hire an inspector who works with investors, not just homebuyers (they look at different things)

- Cover all major systems: foundation, roof, electrical, plumbing, HVAC

- Demand access to attics, crawl spaces, and areas behind finished surfaces—finished basements hide a lot of sins

- For properties built before 1980, consider specialized inspections for asbestos, lead paint, and outdated wiring

- For properties in areas with known issues (radon in certain regions, clay soil shifting foundations), get specialized testing

Don’t hire the cheapest inspector. Don’t rush the process to meet an arbitrary closing date. Don’t waive inspections to beat other offers.

The $500 you spend on inspection is the best insurance you’ll ever buy on a $400,000 asset.

The Problems That Will Eat You Alive

Some repairs are manageable. Budget for them, handle them, move on.

Others will destroy your investment thesis entirely.

Foundation and structural issues top the list. I’ve seen foundation repairs run $30,000-$80,000+ in Canada, depending on severity and region. Sometimes they cost more than the property is worth. And unlike a roof, foundation problems often can’t be fully resolved—you’re managing them forever.

Major system replacements add up fast. In 2026 dollars, you’re looking at:

- Complete roof replacement: $15,000-$30,000+

- Electrical rewiring: $10,000-$25,000

- Full plumbing replacement: $15,000-$35,000

- HVAC system: $8,000-$20,000

A property needing two or three of these simultaneously? That’s a dangerous accumulation of expense that can flip a “deal” into a disaster.

Environmental issues are wildcards. Minor mold remediation might run $3,000-$5,000. Extensive mold through wall cavities? $20,000-$50,000+. Asbestos removal varies wildly based on quantity and location. Some environmental problems simply have no economically viable solution.

Location problems are permanent. A property backing onto railway tracks, in a flood zone, or in a neighbourhood with rising crime has built-in limitations. No renovation fixes proximity to a rendering plant. No amount of granite countertops overcomes a declining area.

Making Your Final Decision

After thorough due diligence, step back and evaluate honestly.

Run the real numbers:

- Total acquisition cost = purchase price + Closing Costs + repairs needed to make it rentable

- Compare that total against the after-repair value

- Project realistic Cash Flow (use actual vacancy rates for the area—not 5% if local vacancy runs 8%)

- Calculate your actual return—does it justify the risk and effort?

Then ask yourself these three questions:

- Can the problems I’ve found be fixed at reasonable cost—and do the numbers still work after those costs?

- Am I excited because this is genuinely good, or because I’ve invested time and don’t want to “lose” the deal?

- If this deal fell through tomorrow, would I feel relieved or disappointed?

That last question reveals more than any spreadsheet. If you’d feel relieved, your gut is telling you something. Listen to it.

When “Problem Properties” Actually Make Sense

Not every property with issues is a money pit. Some become excellent investments when purchased at prices that genuinely reflect the problems.

The difference comes down to this:

- You understand the problems before you buy (no surprises after closing)

- The purchase price actually accounts for repair costs (not just a token discount)

- Post-repair values support profitable operation

- The problems are fixable, not permanent

Buying a property that needs a $20,000 roof in a strong neighbourhood? Fine—if the price reflects that $20,000 and the numbers still work. Understanding the differences between single family and duplex investments can also help you choose the right property type for your risk tolerance.

Buying a property with foundation issues in a declining area for 10% off? You’re buying someone else’s nightmare and calling it a deal.

Frequently Asked Questions

How can I tell if a low price indicates problems?

What are the most expensive property problems to fix?

Should I ever buy a property with known problems?

How do I find a reliable property inspector in Canada?

Can money pits ever become profitable?

Why should I never skip a property inspection even in a competitive market?

What does it mean when a property has been on the market for over 90 days?

The Best Deal You’ll Ever Make

Here’s the truth experienced investors know: the best deal you’ll ever make might be the money pit you didn’t buy.

Every investor I know who’s been at this for a decade or more has walked away from properties that looked promising on the surface but revealed problems under scrutiny. The discipline to say no—even when you’re excited, even when you’ve invested time, even when you really want it to work—protects your capital for opportunities that actually make sense.

Do your homework. Get proper inspections. Trust the red flags when you see them. And get your investment property mortgage pre-approval in place so you’re ready to act when the right deal does come along.

The properties you avoid matter as much as the properties you buy.

Disclaimer: LendCity Mortgages is a licensed mortgage brokerage. Content on this page is for educational purposes only and does not constitute legal, tax, investment, securities, or financial-planning advice. Rates, premiums, program terms, and regulations referenced are as of the page's last updated date and are subject to change. Any investment returns, rental yields, tax savings, or case-study figures shown are illustrative only — they are not guaranteed, not typical, and individual results will vary. Consult a licensed lawyer, Chartered Professional Accountant, or registered dealer before acting on any information above. Editorial standards.

Written by

Scott Dillingham

Published

January 27, 2026

· Updated June 29, 2026Reading time

10 min read

Pre-Approval

A conditional commitment from a lender stating your borrowing capacity, valid for 90-120 days. For investors, getting pre-approved helps you move quickly on deals and shows sellers you're a serious buyer with financing in place.

Cash Flow

The money left over after collecting rent and paying all expenses including mortgage, taxes, insurance, maintenance, and property management. Positive cash flow is the primary goal of buy-and-hold investors. See also [NOI](/glossary/#noi), [Cash-on-Cash Return](/glossary/#cash-on-cash-return), and [Vacancy Rate](/glossary/#vacancy-rate).

Closing Costs

Fees paid when completing a real estate transaction, including legal fees, land transfer tax, title insurance, appraisals, and adjustments. Closing costs affect your total cash invested and therefore your [cash-on-cash return](/glossary/#cash-on-cash-return).

Vacancy Rate

The percentage of rental units that are unoccupied over a given period. A critical factor in [cash flow](/glossary/#cash-flow) analysis, typically estimated at 4-8% for conservative projections. Vacancy directly reduces [NOI](/glossary/#noi).

Due Diligence

The comprehensive investigation and analysis of a property before purchase, including financial review, physical inspection, title search, and market analysis.

Market Value

The estimated price a property would sell for on the open market under normal conditions. Determined by comparable sales, location, condition, and market demand.

HVAC

Heating, Ventilation, and Air Conditioning systems that control temperature and air quality in buildings. HVAC is often one of the largest energy expenses in rental properties, and upgrading to high-efficiency systems can significantly reduce operating costs and increase NOI.

Deferred Maintenance

Necessary repairs and maintenance that have been postponed or neglected, creating a backlog of work that will eventually require attention. Properties with significant deferred maintenance can be value-add opportunities for investors willing to address accumulated issues.

Carrying Costs

The ongoing expenses of holding a property, including mortgage payments, property taxes, insurance, utilities, and maintenance. Understanding carrying costs is essential during renovation periods when the property generates no rental income.

Property Inspection

A professional examination of a property's physical condition, including structural elements, mechanical systems, roofing, and other components, typically conducted before purchase. Thorough inspections help investors identify problems, estimate repair costs, and negotiate purchase prices.

Comparable Properties

Similar properties in the same market area used to establish fair market value or rental rates through comparison of features, location, condition, and recent sale or rental prices. Analyzing comps is essential when determining offer prices and setting competitive rents.

Days on Market

The number of days a property has been listed for sale or rent without being leased or sold, used as an indicator of market demand and pricing appropriateness. Properties with high days on market typically signal pricing issues or property deficiencies.

Real Estate Agent

A licensed professional who represents buyers or sellers in real estate transactions, providing market expertise, negotiation skills, and access to the MLS. Working with an investor-friendly agent who understands rental property analysis and financing strategies can significantly impact deal quality.

Insulation

Material installed in walls, attics, and floors to resist heat flow, measured by R-value. Upgrading insulation in older properties reduces heating and cooling costs, improves tenant comfort, and can qualify for government energy rebates.

Plumbing

The system of pipes, drains, fixtures, and fittings in a building that distributes water and removes waste. Plumbing issues are among the most costly repairs in rental properties, and older galvanized or polybutylene pipes often need replacement during renovations.

Foundation

The structural base of a building that transfers loads to the ground. Foundation issues such as cracks, settling, or water intrusion are among the most expensive repairs in real estate and can significantly impact property value and financing eligibility.

Roof Replacement

A major capital expenditure involving the complete removal and installation of a new roofing system. Roof age and condition are critical factors in property inspections, insurance eligibility, and financing approvals, with typical costs ranging from $5,000 to $30,000+ depending on property size.

Hover over terms to see definitions. View the full glossary for all terms.